Infrastructure

What is infrastructure investing?

Infrastructure is an asset class that emerged in the mid-1990s and has continued to gain greater acceptance from institutional investors over time. The market is now over US$100 billion strong in terms of capital raised per year, with more than 100 funds closed annually.1 Infrastructure is typically considered in a portfolio context alongside other private markets asset classes, such as private equity and real estate. However, infrastructure investments share certain attributes that make them unique and are meant to provide steady, reliable returns across a wide variety of economic conditions. Returns are generally inclusive of a cash yield, which is beneficial for investors who seek income as well as total return.

-

Infrastructure is defined as the basic physical and organizational structures needed for the operation of a society or enterprise. Traditional infrastructure subsectors include social infrastructure (schools, hospitals, etc., typically built under public-private partnership frameworks), utilities (gas, water/waste and electricity networks), transportation (toll roads, airports and seaports) and energy infrastructure (power generation and midstream assets, such as pipelines).

-

-

$1.4 US

trillion

Estimated sum the

infrastructure bill could add to

US economy in next 8 years

Infrastructure Risk and Return Categories

Infrastructure equity investing is typically divided into four main risk categories: core, core plus, value add and opportunistic. These are commonly accepted classifications used by investors to assist in portfolio construction and ensure appropriate diversification when allocating to the asset class. However, these classifications are also affected by factors such as an asset's development stage (that is, brownfield or greenfield2) and geography (that is, developed or emerging market), amongothers.

-

Core infrastructure

This is considered the most stable form of infrastructureequity investing, as these assets tend to be the most essential to society or otherwise largely de-risked (that is, brownfield in nature). Returns are generally derived from income with limited upside through capital gains, and assets are commonly held for the longer term (more than seven years).Revenues and cash flow are generally governed by either rate regulation, availability agreements(which provide for the payment of revenue as long as a facility is able to operate) or long-term contracts with highly creditworthy counterparties,such as governments, municipalities andtop-tier industrialcompanies

-

Core-plus infrastructure

These assets have some similarities with core infrastructure; however, there is generally more variability associated with the cash flows of core-plus assets. Income is still a component of overall returns, but there is also scope for greater capital appreciation. The holding period for core- plus assets is typically more than six years. Core-plus infrastructure still primarily consists of brownfield assets. These assets are typically less monopolistic than core infrastructure and may include a growth/GDP- linked component or some other form of asset or contract optimization.

-

Value-add infrastructure

These investments typically include less monopolistic assets, assets that have a material growth, expansion or repositioning orientation, and certain greenfield assets. The holding period for value-add infrastructure is generally shorter than for core-plus infrastructure and typically ranges from five to seven years. Returns are primarily from capital appreciation rather than ongoing income.

-

Opportunistic infrastructure

These assets that have the highest degree of risk but also return potential. Assets can include those in development, those located in emerging markets, those subject to a high degree of volumetric or commodity price exposure, or those under financial distress and in need of significant repositioning. In general, opportunistic infrastructure assets share many characteristics with private equity investments. Holding periods typically range from three to five years, and returns are almost entirely from capital appreciation.

Infrastructure investment

Characteristics by risk profile

|

Core |

Typical subsectors |

|

Core plus |

Typical subsectors |

|

Value add |

Typical subsectors |

|

Opportunistic |

Typical subsectors |

Environmental, Social

and Governance (ESG) considerations

ESG is an important topic within infrastructure. Many infrastructure assets have a large environmental footprint, and most, if not all, have a direct social impact on the stakeholders within theregions in which they are located. Governance is also important, considering that holding structures may be complicated and many assets have concessions, contracts or agreements with governmententities. Accordingly, we view ESG as a critical issue that all infrastructure managers should address to execute their investment strategiessuccessfully.

In short, we believe ESG is a critical component of infrastructure investing, and it's something we carefully consider when performing due diligence on private markets investmentmanagers.

-

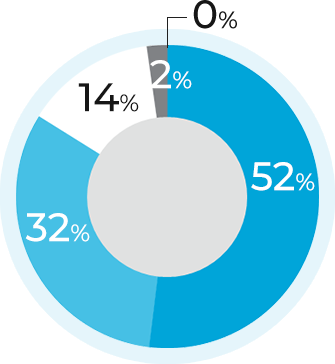

When contemplating investing in a US infrastructure project,

how important are ESG considerations?

Very unimportant Somewhat important Neutral Somewhat unimportant Very unimportant -

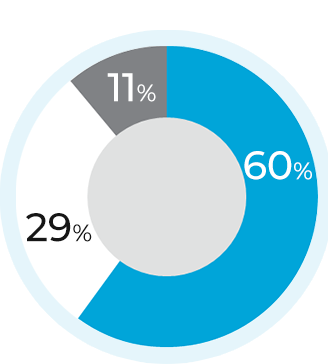

When contemplating investing in a US infrastructure project,

how important are ESG considerations in comparison to

investing in a project in an emerging jurisdiction?

More important About the same Less important

-

The focus has to shift from

highway development and

move on to the more

future-ready sectors

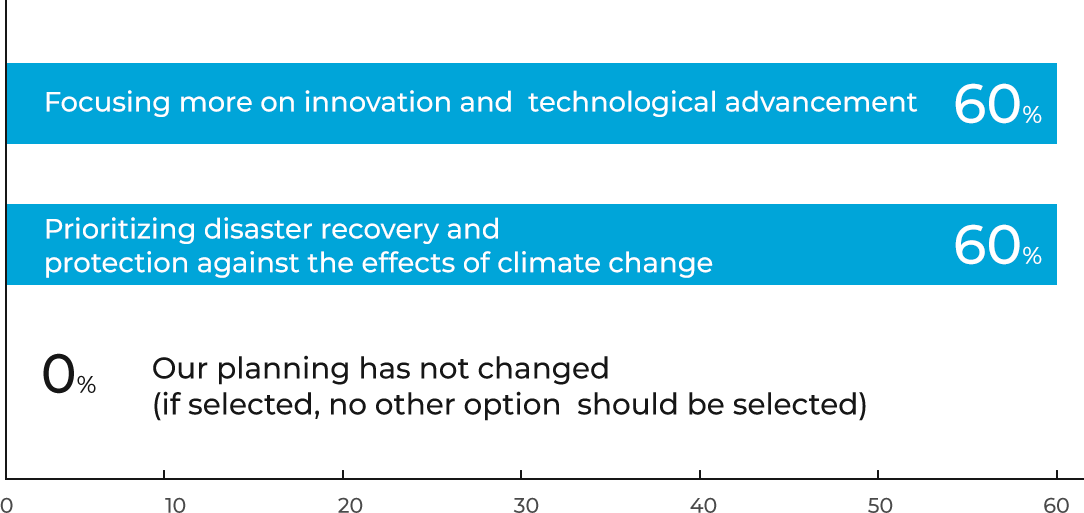

Is your organization making any of the following changes to

accommodate climate change and weather risk in the US?

-

Only investing in states and territories where disaster recovery and protecting against the effects of climate change are a priorityOur business model has not changedFocusing on innovation and technological advancementOnly investing in states and territories where these factors are a low risk

Is your organization's infrastructure planning changing to

accommodate climate change and weather risk in the US

in either or both of the following ways?

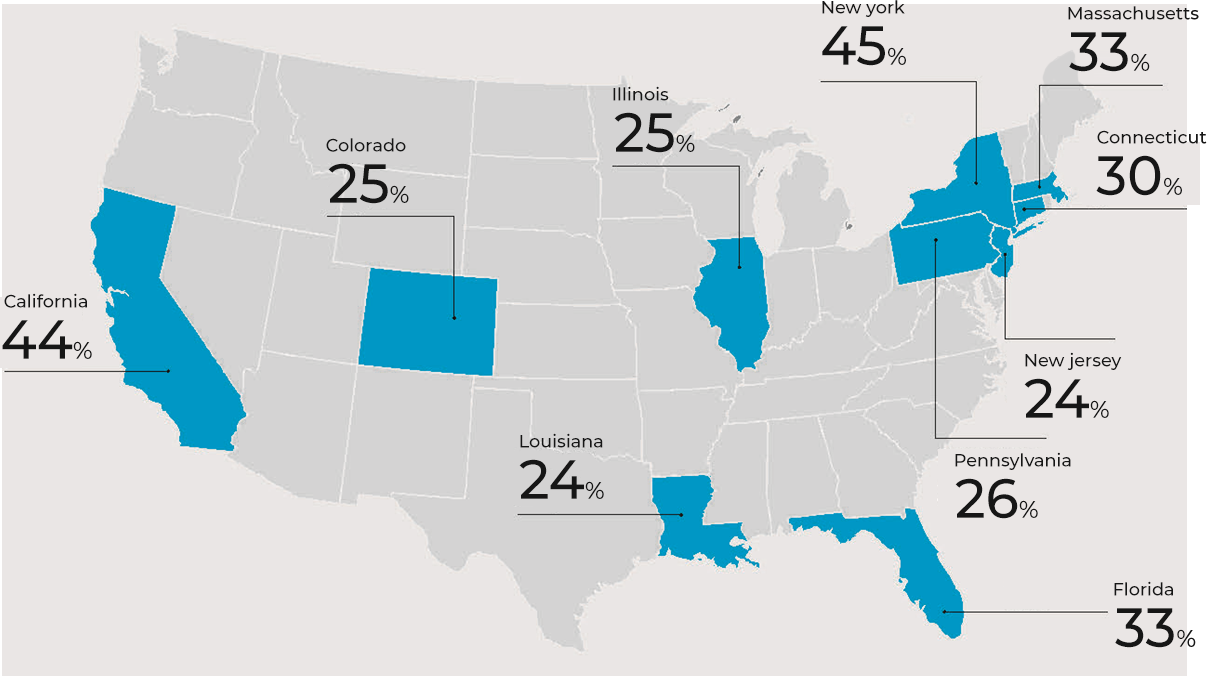

In which US states and territories do you plan to invest in

infrastructure over the next year?

In which US infrastructure sectors do you plan to invest in 2022?

-

-

Roads, tunnels, bridges

65%

-

-

Social (educational. healthcare, aged care)

55%

-

-

Energy transmission and distribution

42%

-

-

Water (supply and treatment)

40%

-

-

Telecommunications

40%

-

-

Ports and marine

39%

-

-

Airports/Aviation

38%

-

-

Waste treatment and recycling

35%

-

-

Rail (passenger)

33%

-

-

Rail (freight)

30%

-

-

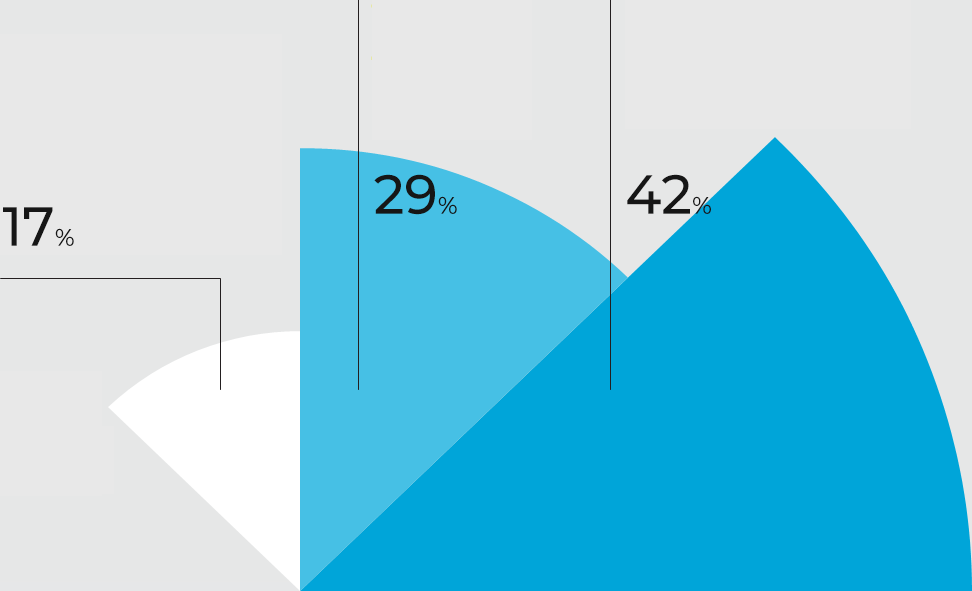

Solar (CSP/PV)

29%

-

-

Offshore wind

29%

-

-

Other renewable energy (biomass, etc.)

28%

-

-

Digital-Towers

28%

-

-

Fossil fuels (e.g., coal and gas)

24%

-

-

Digital - Date centers

24%

-

-

Carbon-capture, utilization or storage

23%

-

-

Digital - Fiber to homes

23%

-

-

Other transit

21%

-

-

Onshore wind

20%

-

-

Altermative fuel distribution

20%

-

-

Battery storage

19%

-

-

Gray hydrogen

17%

-

-

Clean hydrogen (green/blue/pink)

16%

-

-

EV charging infrastructure

16%

-

-

Pipelines

14%

-

-

Nuclear

6%

-

-

Other storage

5%

Potential Risks to Consider

Although there are several potential benefits associated with investing in infrastructure within a traditional portfolio, there are still certain risks that investors should consider. The below list is not exhaustive; however, we believe it includes some of the most pertinent risks associated with infrastructure investing.

-

01

Liquidity risk

Private markets infrastructure investments are considered to be illiquid and may not be saleable at the time an investor had originally planned for exit. Having a long-term investment strategy and maintaining appropriate levels of liquidity on a total portfolio basis are methods that can be used to manage illiquidity risk at the total portfolio level.

-

02

Vintage year risk

Returns for closed-end infrastructure funds may vary due to vintage-year effects of investing and divesting assets across various economic environments. Investors can diversify against vintage-year risk by building out a portfolio over a three- to five-year period, which will allow the portfolio to be constructed throughout various points in an economic cycle.

-

03

Blind pool risk

Investors allocating to closed-end private markets infrastructure investments allocate to 밷lind pools?in which the manager has full discretion to build out the portfolio. There is a risk that the investment manager may construct a portfolio differently from how the strategy was marketed.

-

04

Environmental risk

Many infrastructure investments, such as oil and gas midstream assets or conventional power generation, have environmental footprints that must be managed. Failure to do so may result in some combination of land, water or air contamination. The costs associated with an environmental breach include not only remediation but also potential fines and future operating restrictions. There is also the risk of future regulatory changes negatively affecting the conventional power sector.

-

05

Legal compliance and regulatory risk

Infrastructure assets are subject to numerous laws, statutes and regulations. Compliance failures can result in fines, restrictions, increased scrutiny and, at the most extreme, a revocation of the license to operate an infrastructure asset. It is also possible that future laws and regulations may change, which is a risk for which investors need to be prepared.

-

06

Operating and technical risk

Infrastructure investments are often complicated assets or businesses that have unique characteristics. Operating risk is concerned with a business not functioning in an efficient manner. Technical risk is concerned with a design flaw or inadequate resource assessment that can impair an asset's overall ability to operate as intended.

This primer provides an overview of the characteristics of private markets infrastructure, which we believe is an asset class that offers a compelling blend of risk and return characteristics to investors seeking to diversify and enhance portfolios. Please contact your Genesis representative to discuss this primer further and for assistance in developing an infrastructure investment program.